How to Get Better Regular Monthly Income for Retirees

It is observed that quite a few retirees who do not get pension are quite worried about gradually but surely falling interest rates on Bank Fixed Deposits on which they depend on the regular quarterly / monthly income. Even if they opt for investing money in ‘Senior Citizen’s Savings Scheme (SCSS) & ‘Pradhan Mantri Vaya Vandana Yojana’ (PMVVY) and get a sort of quarterly / monthly income similar to pension there are certain limitations for the maximum amount to be invested in each such scheme i.e., Rs. 15,00,000/- each. And the ROI at present for these schemes is only @ 7.40% p.a. which eventually, most likely will be reduced after the stipulated lock-in period expires. The said income is also ‘taxable’ in the hands of the recipient. After the expiry of the scheme time the same amount originally invested will be returnable to the investor at par. Thus, by investing a total amount (maximum) of Rs. 30,00,000/- theoretically one will get a taxable monthly income of only Rs. 18,500/-.

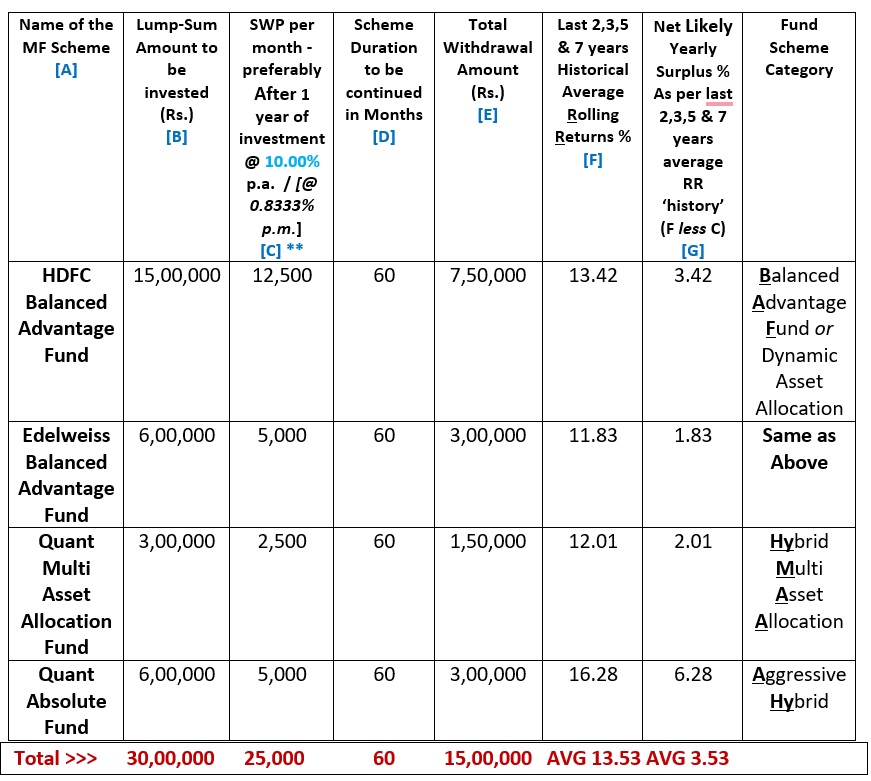

Now consider this option to generate a better average monthly income @ 10.00% p.a. (instead of @ 7.40% p.a. as above) with quite a possibility of increase in the originally invested corpus amount at the end of the period. In this scenario, the investor will be required to take a calculated risk of investing the money in certain open ended ‘Hybrid Mutual Fund’ Schemes with “Direct – Growth” as default option. The detailed methodology is narrated below step-by-step. Please see the table below >

Now let me first explain what is the meaning of ‘Fund Scheme Category’ in brief and the ‘Risk’ involved therein.

Now let me first explain what is the meaning of ‘Fund Scheme Category’ in brief and the ‘Risk’ involved therein.

Balanced Advantage Fund/ (Dynamic Asset Allocation): —

In the said scheme asset allocation between the two asset classes equity & debt is managed dynamically on the prevailing Stock market condition as such it carries relatively low risk of market volatility / drawdown. BAFs sell stocks in their portfolio when valuations are high and do the opposite when markets crack. Such a quick, effective, and conservative investment strategy helps the investor handle the market volatility quite comfortably. Thus, investors get the optimum benefits of both asset classes – debt and equity. At a time when equity valuations are not cheap with key indices trading at an all- time high, a Balanced Advantage Fund could be a good choice. These funds not only reduce the downside when markets fall but also help investors make the most of a full market cycle. For existing investors in equity mutual fund schemes or new investors who are jittery looking at the current market levels but at the same do not want to lose out on any further rise in stocks hereon, BAFs may be worth investing in. Every AMC has their own set of methodology / various parameters to determine the quantum and timing of AUM to be invested ‘dynamically’ between equity and debt depending on their perception about the current / future likely state of the Stock market.

Hybrid Multi Asset Fund: —

The AUM of the fund is invested more tilted towards equity or equity related instruments but also in debt. Further it also takes exposure in ‘commodity’ (Gold) to a certain extent as hedge for stock market volatility.

Aggressive Hybrid Fund: —

The AUM of the fund is invested more tilted towards equity or equity related instruments but also in debt.

In view of the above it may be noted that about 70% of our ‘corpus’ is invested in BAF category which relatively carry low risk and only 30% is invested in HYMAA & AHY category which carries rather higher risk. Thus, getting inflation beating more monthly returns with most likely increase in corpus at the end justifies taking a little calculated risk. Please note if you are totally averse to take “any” risk you will surely find yourself in serious financial trouble going forward.

Now we come to the actual process of one-time investment and systematic withdrawal plan (SWP) to be carried out on regular monthly basis.

{A} Firstly, you will need to open a DMat cum Trading Account either with www.kuvera.in OR www.zerodha.com (coin. zerodha platform) by following their ‘New A/C opening procedure’. You will be able to ‘Buy’ and ‘Sell’ your desired MFs on-line directly without involving any other intermediary broker / commission agent and save your brokerage / commission as they do NOT charge anything on such transactions. It may please be specifically noted that AMCs provide better NAV to ‘direct’ investors than to those who invest through other regular brokers / commission agents. Thus, there is a good amount of money ‘saving’ made in the entire life span of the scheme as there is NO payment of such money to others out of your (investor’s)pocket.

{B} Always opt for “Growth” option and never go for “Dividend” option.

{C} Please wait for one (1) year for any monthly ‘withdrawal’ after the initial lump-sum investment is made. This will avoid you paying likely ‘Short Term Capital Gain Tax’ which is more than ‘Long Term capital Gain Tax’. But if you start your SWP immediately say after only 1 month of lump sum investment you will need to pay ‘Exit Load’ and also ‘Short Term capital Gain Tax’ if applicable.

{D} Preferably, only after 1 year of initial lump-sum investment start / opt for monthly ‘Systematic Withdrawal Plan’ (SWP) preferably determining the withdrawal date as 27th of the month.

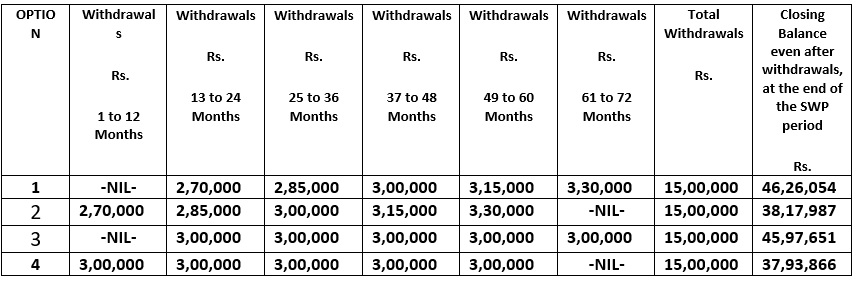

{E} The monthly withdrawal amount should ideally be not more than 0.8333% p.m. Of the initially lump-sum invested amount in the scheme and continue it at least for next 5 years (60 months) OR alternatively one can withdraw per month gradually increasing amount (which will partially take care of inflation) with a gap of every 12 months i.e., First 12 months @ 0.75% p.m., Next 12 months @ 0.7917% p.m., Next 12 months @ 0.8333% p.m., Next 12 months @ 0. 8750% p.m. and last 12 months @ 0.9167% p.m. As per the standing instructions given in the SWP mandate the said amount will be automatically get credited to your Bank A/C by month end regularly on monthly basis as if you get pension. Alternatively, if there is no such automatic SWP facility available on the said platform then, with little more effort one can easily withdraw the predetermined amount every month as shown in column ‘C’ ** from each MF. At the end of 5 years of withdrawals, you will most likely find the increased total corpus amount than what is initially invested as summarized below. Choose your ‘option’ as per your requirement judiciously.

{F} Please ensure to file your IT Return every year properly and in time after taking in to consideration Short / Long Term Capital Gains, resulted out of SWP as mentioned above. >>> STCG / LTCG, as the case may be.

Article Compiled & Written By/-

Prakash P. Joshi Ex Banker, Financial Consultant & Freelance Educator Vile Parle (East), Mumbai – 400057, INDIA. |

|

| WhatsApp Mobile > | +91- 9920334762 |

| E- Mail > | ppjoshi49@gmail.com |

**** MONEYSMART ****

DISCLAIMER

It may please be noted that the above script is for information purpose only and the same shall NOT be construed as advice and / or guidance for investment in any manner